Meassuring Firm Performance

- The Balance Sheet: is a snapshot of a firm’s financial position at a particular point in time (normally the last day of accounting period). It summarizes assets, liabilities and owners’ equity.

- The Income Statement: summarizes revenues and expenses over a period of time. (revenues, expenses, profits before taxes, taxes paid and profits after taxes)

- Financial Performance ratios (Key performance indicators)

The Balance Sheet

- Every organization has assets and liabilities Assets

- Assets are items to which the organization has legal title

- Current assets can be converted into cash within 1 year

- Fixed assets have a life greater than 1 year Liabillities

- Liabilities: debt owed (suppliers, employees, government)

- Current Liabilities debt normally paid within a year (accounts payable, taxes, wages, bank loan, …)

- Long-term liabilities debt normally paid beyond current year Owners Equity

- Owners’ Equity: The difference between assets and liabilities is a means of measuring what the organization is worth – it’s equity:

- Owners’ equity often appears as two components in a balance sheet:

- Stock: par value per share, also known as nominal or original value, is the face value of a bond or the value of a stock certificate, as stated in the corporate charter

- Retained earnings: the amount of net income left over for the business after it has paid out dividends to its shareholders

The Income Statement

- Income Statement summarizes revenues and expenses over a specified accounting period (Month, quarter, and year)

- Major components: Revenues, Expenses, Profits

- Revenues: from sales of goods/services

- Expenses: cost of goods sold, rent, insurance, wages, depreciation

- Income or profit before taxes: Revenues – Expenses

- Net income (profit): Income (profit) before taxes – taxes

Estimated Values in Financial Statements

- Financial statements are often estimated: they may not reflect market values

- Assets are valued on the basis of their cost (book value)

- Land is listed at the price paid - not its market value

- Plant and equipment is listed at the price paid less accumulated depreciation

- Depreciation on equipment computed using a depreciation model

- Stock or Shares are listed at par value (issue price)

- Finished goods inventory – manufacturing cost

- Most firms include their accounting methods/assumptions

- within periodic reports to aid interpretation of statements

Financial Performance Ratios

- Decision makers (inside and outside) need to know general performance of a firm

- Balance sheet/income statements are used for assessment

- Financial Ratio Analysis : key performance indicators

- These performance measures are financial ratios calculated from items on the income statement and balance sheet.

- In interpreting ratios, analysts should calculate the ratios over a number of periods to do a trend analysis

- Ratios should also be compared to industry standards

- Industry standards routinely published by commercial and government websites/publications (Statistics Canada)

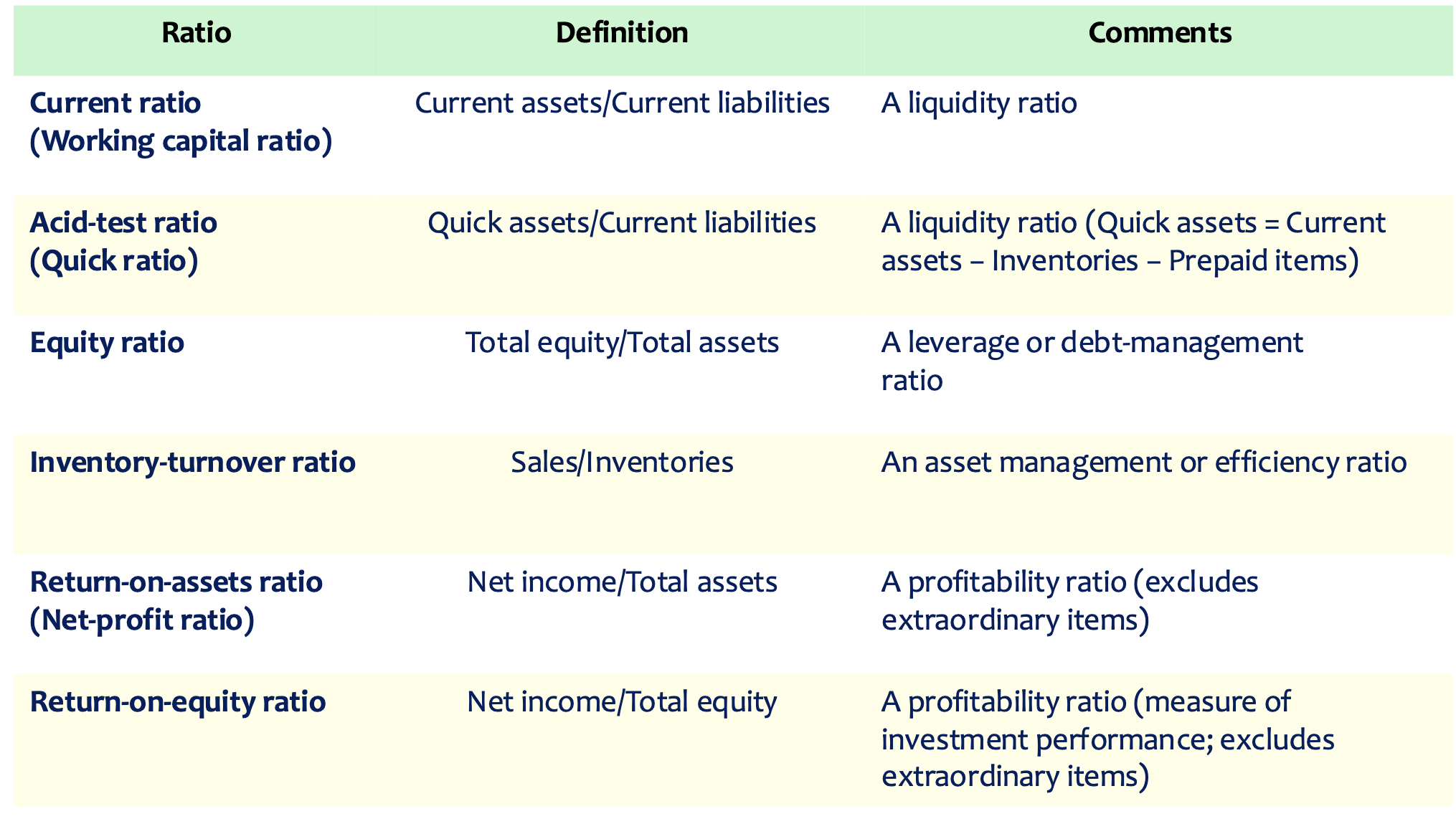

Financial Ratios

- Liquidity ratios: firm’s ability to meet short term financial obligations

- Company’s net reserve of cash and assets that easily can be converted to cash is called working capital.

- Working capital = current assets − current liabilities

- The adequacy of working capital is measured with two ratios:

- Current ratio

- Acid-test ratio (Quick ratio)

- A current ratio of 2+ is adequate

-

- Where quick assets are assets that are quickly convertible to cash

- Cash, accounts receivable, notes receivable, temporary investments in the market

- Inventory is not a quick asset

- An acid-test > 1 is adequate

- Where quick assets are assets that are quickly convertible to cash

- Debt Management Ratios: the extend to which a firm relies on debt for its operations

- : this is a measure of financial strength

- Debt ratio < 0.2 or less indicates sound financial condition

-

- The smaller the ratio, the more dependent a firm on debt and the higher risk of not being able to manage debt

- Comparison to industry norms/trend analysis necessary

- Efficiency Ratios: assess efficiency of use of its assets

-

- The total sale in a period divided by the value of average inventory level at the same period by the average selling price

- A higher ratio points to Strong sales and a lower ratio to weak sales

-

- Profitability Ratios: How productively assets have been employed in producing a profit?

Business Plan

A 3-5 year road map of a business

- Outlines operating, marketing, financial and HR status and intensions

- Identifies the nature and feasibility of the business considering financing options and forecasts cash flows

- Drafting a good BP is an essential step in starting a business

- Balance sheets, income statements and financial ratios are used in a BP to analuze the financial status of the company

Aspects of a Business Plan

- Executive summary

- Convinces investors to read further

- Primarily convinces reader of future success

- Features the mission statement, provided products and services, overall financial health, future plans

- Company Description

- High level overview of company and operations

- Products / services and market needs

- Company HR capabilities

- Competitive advantages of the company

- Market Analysis / Future Outlook

- Description of industry and growth plans of company

- Market demand: discussion of target market

- Future trends: customer demand, technology and market share

- Market share: present / future share compared to competitors

- Weaknesses and strengths

- IT and technology advances

- Geographical location

- Financial situation

- Experience and human factors

- Pricing, revenue and cash flow predictions

- Regulatory environment

- Management and Organization

- Explanation of structure of business in detail

- sole proprietorship, partnership or corporation

- Key corporate employee information provided

- Experience, education, qualifications

- Functional groups, corporate structure, job titles

- How this structure suits corporate mission and future growth

- Explanation of structure of business in detail

- Funding Requirements

- Discussion of where the funding will originate

- Owners and investors

- Banks and other financial institutions

- How company will attract investors for new projects or expansion

- Discussion of where the funding will originate

- Sales and Marketing

- Strategies to penetrate target markets

- Creation / maintaining of customers

- Recognition and fulfillment of needs

- Communication mechanisms (surveys, advertisements) promotions